Insights Blog

Objectives-Based Investing: The Intersection of Planning & Portfolio Construction

June 10th, 2026 // Jack LaLiberte

What is Objectives-Based Investing?

Traditionally, and even to this day, many view the financial advisor as an expert in security analysis, deftly shepherding their clients from one hot stock to the next. At Journey Wealth, we take a distinctly different view of what defines a valuable financial advisor. Although we monitor markets and make thoughtful adjustments when appropriate, an advisor’s real value lies in constructing a goal‑oriented allocation that helps clients stay invested across all market environments.

Objectives-based investing re-frames the capital allocation discussion. Instead of attempting to prognosticate around which market segments are likely to outperform over a certain time-frame, objectives-based investing seeks to construct a portfolio with your unique goals in mind. Rather than chasing the highest possible return, an objectives-oriented investor seeks to optimize risk-adjusted returns and maximize the likelihood of achieving their financial goals.

The Bucketing Concept

The concept of “bucketing” lies at the heart of objectives-based investing. Bucketing simply involves adjusting the risk level for different asset pools based on their assigned purpose. Take the example of a young couple: they are likely saving and investing for multiple goals simultaneously. The allocations for those buckets are determined based on the respective timeline for each goal as well as their risk tolerance. For example:

- If the client has a near-term goal (1-3 years), such as a home purchase, the allocation for that bucket would likely be very conservative, depending on the flexibility of the goal. That portfolio would likely include a large allocation to money market funds or short-term bonds. An inflexible expenditure, such as a looming tax bill, is likely to be allocated extremely conservatively, whereas a goal with a flexible deadline may incorporate a bit more risk.

- A longer-term objective, such as building a retirement nest egg, allows for a riskier, more growth-focused allocation. Notably, the allocation is determined by the client’s unique timeline and the planning constraints, rather than the advisor’s prognostication around short-term market trends.

Objectives-Based Investing & Planning

At Journey Wealth, rather than leading with flashy investment products, we start with planning. The first step in most client relationships is to gain a thorough understanding of your unique financial circumstances, goals & objectives. We believe that it’s irresponsible to propose solutions before fully understanding all aspects of a client’s starting point and desired outcome. As part of that discussion, we also seek to develop an understanding of a client’s risk tolerance. How much volatility are you willing to accept in exchange for the potential to earn higher returns? The answer isn’t formulaic, it’s highly personalized.

Only after deepening our understanding of your personal goals can we begin to allocate your assets. During our planning process, we determine what rate of return is required for you to achieve your goals. Once determined, we adjust our approach based on your personal preferences and appetite for risk. Our approach generally falls into two categories, depending on your personal preferences:

- Risk minimization approach: Once your required rate of return is determined, we use conservative capital market assumptions to design an allocation that we believe will achieve your goals while taking the least risk possible.

- Wealth maximization approach: Some clients have a high risk tolerance and a desire to leave as many assets as possible to their heirs. In this case, it may make sense to segregate a pool of assets and assign a growth focus, while retaining the assets needed for personal financial success in a less-risky pool.

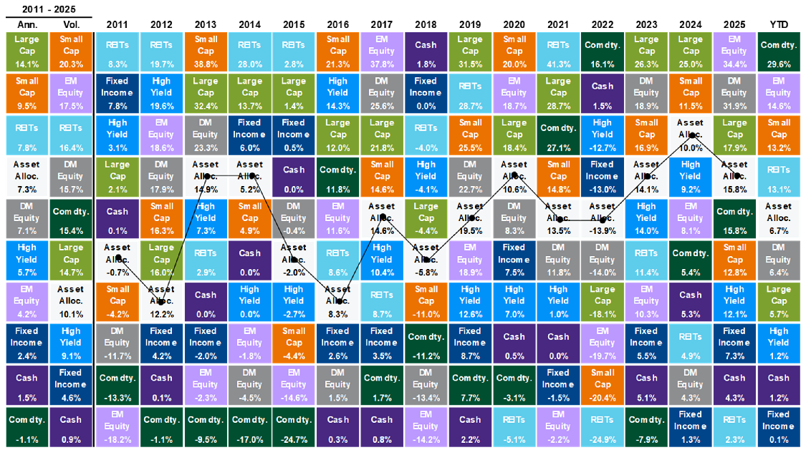

Why Doesn’t Market Timing Work?

The chart below illustrates the futility of trying to anticipate which segment of the market will perform the best in any given year. The lack of predictability is why we don’t attempt to time markets and instead utilize an objectives-based framework for constructing portfolios.

Why Investors Under-Perform?

The average investor has historically under-performed a broadly diversified portfolio dramatically. In fact, the average investor tends to under-perform even within asset classes. Why is that?

- Emotional decision making: Investors are human and, as such, are emotional creatures. The human element often drives investors to allocate capital when they see others making money and pulling back from risky assets when markets are volatile, exactly the opposite of the “buy low, sell high” approach. Investing systematically and having a plan are two of the greatest defenses against emotional decision-making.

- Overconfidence & excessive trading: Many investors suffer from the delusion that they can beat the market. That mistaken belief can lead to concentrated positions and excessive trading activity. These behaviors often lead to inferior risk-adjusted returns and potential tax-drag.

- Trend Chasing: Investors tend to purchase assets that have performed well recently. It’s tempting when a friend touts their carefully curated investment success stories to want to get in on the action. They often fail to mention the less successful investments. However, over a lifetime of investing, nearly all investors would be better off allocating to a diverse basket of securities in a systematic way.

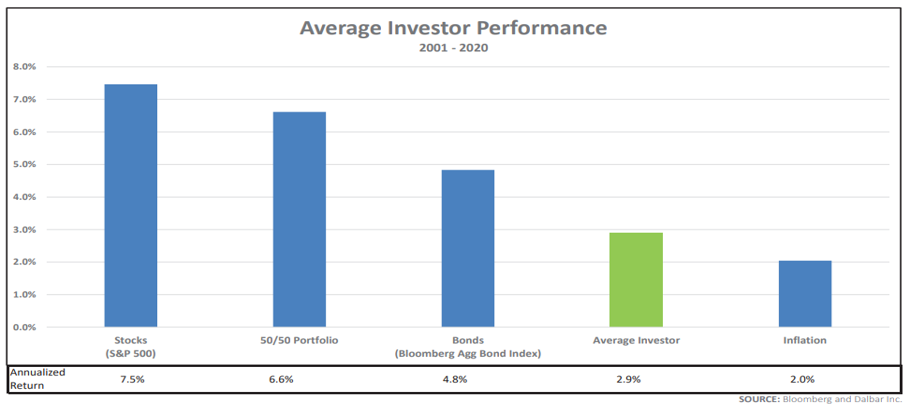

The Folly of the Average Investor

The chart below illustrates the poor performance of the average investor relative to different asset classes as well as a blended allocation. The typical investor’s quest for outsized returns is, ironically, the biggest hindrance to achieving market-like performance. This chart also doesn’t account for risk. The average investor is often taking more risk to achieve inferior returns.

How Do You Avoid These Pitfalls?

- Start with the plan: When you let planning drive decision-making as opposed to emotions or market forecasts, the investment implications become obvious. The portfolio allocation is simply a tool to help achieve your goals.

- Invest regularly & systematically: Most Americans invest regularly by default in their 401k accounts. Developing a target allocation that fits your plan and automating your investing journey shifts the investor mindset. Market dips become opportunities and the stressful process of deciding “when” and “what” to invest in becomes a relic of the past.

- Focus on YOUR goals: Many investors get sidetracked in the comparison game, particularly when the markets are doing well. Rather than comparing your returns to your neighbor’s returns or an arcane index, compare them to your target return levels. If you are achieving the returns specified by your plan over long periods, the process is working.

- Control the controllables: We can’t control the Fed or the markets. We can’t anticipate the next wave of tariff threats or technological disruption. We can control, at least to an extent, our savings habits, investing discipline and our reactions to volatility. While it may not have the same sheen as a fancy investment product, most wealth is built through discipline and consistency rather than by timely tactical investment shifts.

Pulling It All Together

These concepts may seem rudimentary, but they are powerful in their simplicity. Some market commentators and advisors spend considerable time analyzing short-term market trends and prognosticating around which asset class will outperform over some arbitrary future period. We believe that attempting to time the market is a game that cannot be consistently won, even by very intelligent people with access to the best data.

Rather than centering your investment strategy around chasing trends, we believe that a superior approach is to build your asset allocation around your goals and timelines. At the end of the day, most successful investing isn’t about finding an undervalued, overlooked opportunity. The keys to successful long-term investing are consistency, simplicity and repeatability. An objectives-based framework, in conjunction with a detailed financial plan, provides a roadmap for where the next incremental investable dollar should go and how it should be invested, regardless of the latest market noise.

The age of constant, often contradictory, information that we live in makes investing more difficult. It can be agonizing to pull the trigger on investing at times when your phone and television are constant sources of anxiety around the state of the world and the market outlook. By adopting an objectives-based investing framework, you empower yourself to invest based on the requirements of your financial plan, rather than speculation around the future path of markets.

Disclosure: This information was prepared by FSM Wealth Advisors, LLC d/b/a Journey Wealth Management, LLC, a federally registered investment adviser under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply a certain level of skill or training. Neither the information presented nor any opinion expressed herein should be construed as personalized investment, financial planning, tax, or legal advice. For advice specific to your situation, please consult an appropriately qualified professional adviser(s). Certain information herein may have been obtained from various third-party sources; Journey does not guarantee the accuracy or completeness of such information. Investing involves the risk of loss and investors should be prepared to bear potential losses. Past performance is not indicative of future results.

Quarterly Market Commentary

Equity markets in 2026 resemble a revolving door, with leadership regimes swinging wildly from small caps to value and then to growth equities. The rapid rotations we’ve witnessed over the past six months demonstrate the futility of attempting to time equity markets.

Four Pillar Friday

Stories, research, and reflections on how we spend our most important currency: TIME

Four Pillar Friday

Stories, research, and reflections on how we spend our most important currency: TIME