Insights Blog

Mid-Quarter Market Commentary

August 25th, 2025 // Jack LaLiberte

Market Recap

Since the turmoil in April, markets have largely shrugged off indications of a weakening consumer and continued tariff uncertainty. While the speed and magnitude of the decline in US equities in April was jarring, the recovery was also swift. Currently, the lofty valuations and high degree of concentration present in the S&P 500 leave US equities vulnerable to negative surprises. While employment remains stable, the domestic consumer has weakened, and corporate investment has slowed due to uncertainty around global trade. International equities continue to offer a compelling opportunity due to reasonable valuations, broader diversification and intriguing growth tailwinds. The Fed appears more amenable to rate cuts after some weaker employment figures. However, the uncertainty surrounding the impact of tariffs is likely to moderate the pace of cuts. An ample supply of government debt, along with investor hesitance to extend duration in the face of an uncertain environment, are likely to maintain a floor on longer-term bond yields. While predicting the precise path and impact of trade policy is impossible, volatility is likely to persist as markets adjust to elevated levels of uncertainty.

Looking Ahead

Volatility is likely to continue as shifting trade dynamics and a re-calibration of lofty valuations are digested by market participants. However, global fundamentals remain stable. Given the level of concentration within US equity markets, we believe that international, value and small-cap equities provide a critical element of diversification. Fixed income offers a meaningful yield improvement for cash-heavy investors and is playing its intended role as a volatility mitigator during periods of elevated uncertainty. We advocate building portfolios to achieve your long-term goals as opposed to trying to predict the next market-moving event. No one can reliably predict the next trade development or geopolitical shock. We prefer to allocate time to reviewing your personal financial plan and ensuring that your investments align with your goals. Please don’t hesitate to reach out to your advisor to schedule time to discuss your financial plan, including your goals and planning assumptions.

Leading Topics

Tariffs & The Economy

As of mid-August, 10% universal tariffs on imports have been imposed, along with higher rates on certain countries and categories. The impact remains difficult to assess, largely due to uncertainty over how long tariffs will remain in effect. Likely impacts include demand reduction as consumers adjust spending to offset higher prices on goods as well as reduced capital investment by firms due to elevated uncertainty. Employment figures remain steady but hiring has slowed. While trade uncertainty is disconcerting, long-term growth and demographic trends are likely to have a far greater influence on future returns. The consumer was already showing signs of strain before tariff implementation. The combination of tariffs and a limited political appetite for meaningful deficit reduction is likely to sustain elevated inflation and higher long-term yields.

Federal Reserve & Interest Rates

The Fed has kept rates steady since the end of 2024, citing stubborn inflation, a healthy labor market and the unknown impact of tariffs on price levels. Futures markets are currently pricing in two to three rate cuts for 2025, though that could be tempered if inflation remains persistent. Long-term rates are likely to remain elevated regardless of the Fed, potentially hampering corporate investment and consumer spending.

Fixed Income

Given investor concerns around inflation and substantial government debt issuance, we expect long-term rates to remain elevated. There is a meaningful yield advantage in core fixed income relative to cash. Although cash can be a tempting haven in periods of uncertainty, it has historically underperformed fixed income in most market environments. This has held true thus far in 2025, with fixed income dramatically outperforming cash, even with volatility in interest rates. While bond investors still bear the scars of 2022, the yield environment is very different today. Investors are receiving substantial compensation for owning fixed income relative to cash. That additional yield helps insulate investors from volatility in interest rates, while cash yields are likely to remain the same or decline depending on the Fed’s actions.

Equities: Valuation & Concentration

Elevated valuations and concentration in US equities make them vulnerable to negative surprises. The S&P 500’s valuation has climbed well above the long-term average, particularly when higher interest rates are factored into the discounting of future earnings. While the bulk of returns have been generated by a narrow segment of the equity universe over the past decade, returns tend to be more broad-based when interest rates are elevated. The combination of favorable valuations, a weaker US growth outlook and shifts in global trade dynamics make international equities particularly appealing. We recommend reviewing your equity exposure and diversifying to less richly valued segments, including value, small-cap and international equities.

Economic Fundamentals: Higher Uncertainty, Slower Growth

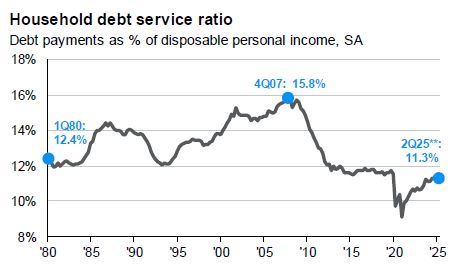

Consumer spending represents the bulk of US GDP. Over the past few years, excess savings built up during the COVID era have been depleted and wage growth has slowed considerably. The cumulative strain of years of elevated inflation has driven many consumers to lean on high interest auto loans and credit cards to close funding gaps. While consumer debt service ratios are consistent with the pre-COVID period, delinquencies have dramatically increased over the past few years. Flows into delinquencies for credit cards and auto loans are at levels not seen in over a decade. It’s now estimated that the top 10% of households account for about 50% of US consumer spending. As net savers, those wealthier households are less vulnerable to higher rates. However, households with more robust balance sheets may be susceptible to the wealth effect. Given weaker transaction activity in real estate and private equity markets, wealthier households may adjust spending, further pressuring the largest component of GDP.

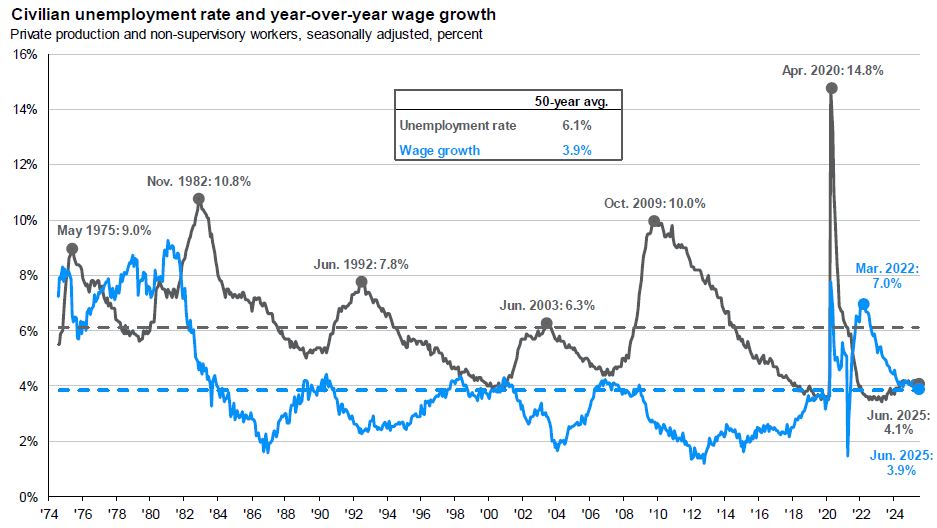

The US labor market remains stable but weakening. Layoffs haven’t materially increased over the past few years. However, employers have dramatically pulled back on hiring, as evidenced by job openings at around half of their 2022 levels. Revisions to recent monthly payroll data also indicate slow but positive growth in employment. While the labor market has deteriorated since the COVID era, the unemployment rate remains historically low. In addition to a weaker consumer, business investment has declined sharply over the past two quarters. The elevated uncertainty surrounding global trade dynamics is likely to continue to hamper business investment. While US GDP growth is far from recessionary levels, the downward trend is worth monitoring closely over the coming quarters.

Tariff Update

As of mid-August, the US has imposed a 10% tariff on nearly all imports, with some exceptions. There are more substantial tariffs in effect on certain countries and sectors, including China and Canada. Additional tariffs have been threatened but suspended. While headline GDP rebounded in the second quarter, this was largely due to a reduction in imports after many were pulled forward to the first quarter. Excluding the impact of net imports and the reduction in business inventories, second quarter GDP expanded at an annualized rate of 1.2%. While that represents a deceleration from recent quarters, it’s far from a recessionary level.

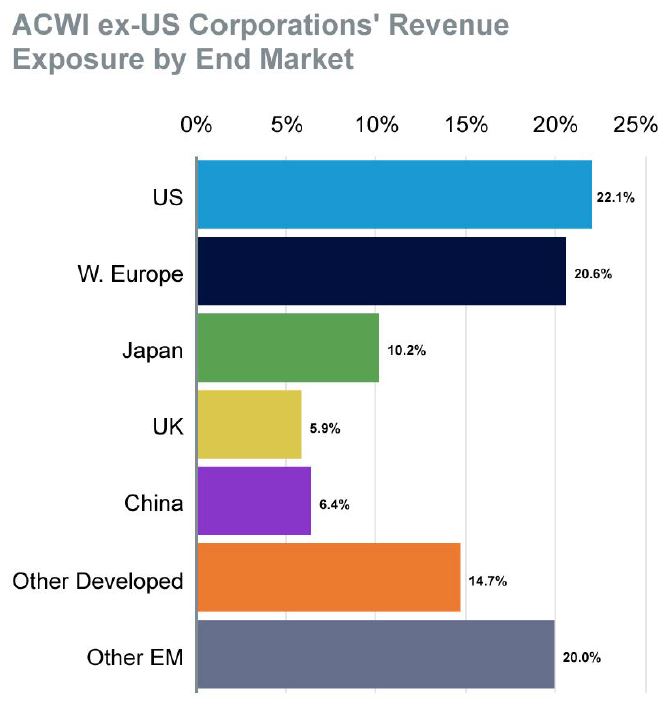

The impact of tariffs on equity markets is difficult to forecast, given the ever-changing proposals on the table. However, the increase in uncertainty is likely to constrain investment and damage domestic demand. At a sector level, industrials and consumer cyclical companies are particularly susceptible to volatile trade dynamics. Financials are likely one of the sectors that is more insulated from tariff risk. Mexico and Canada are some of the most vulnerable countries, as they depend heavily on the US for trade. However, most countries have diversified their trade networks, with the US accounting for an average of about 22% of revenue for foreign companies. While nearly all US companies need to adjust to changing trade dynamics, many foreign firms have minimal exposure to US trade. On the fixed income front, higher inflation expectations, which are partially driven by tariffs, are likely to maintain a floor on long-term yields. A steeper yield curve is a hindrance to long-term borrowers, such as homebuyers, but could present an opportunity for fixed income investors.

Equity Markets: Valuation & Concentration

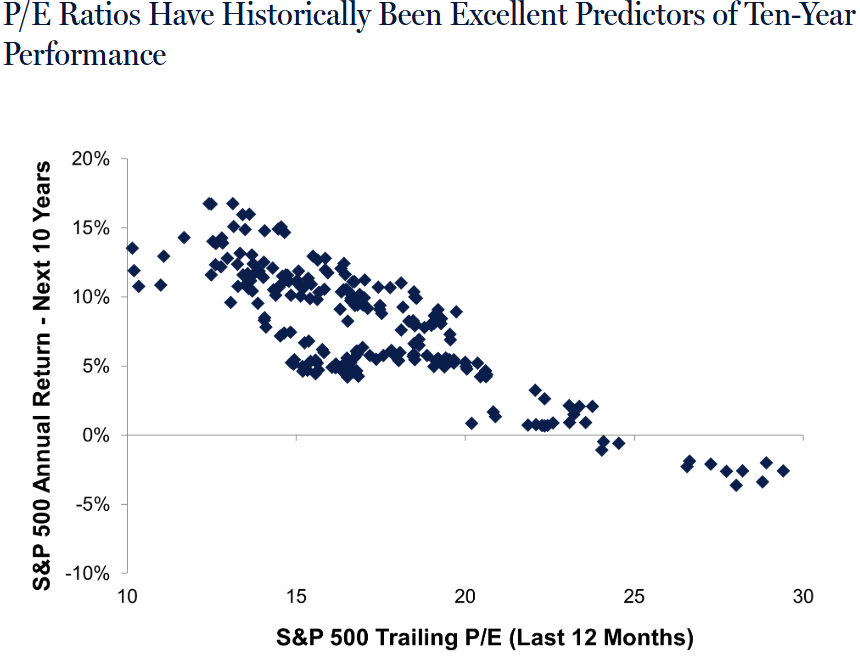

Since April’s volatility, US equity markets have executed the most rapid recovery from a decline of 15% or greater since 1957, bringing elevated concentration and valuation levels back to the forefront. Current valuations, particularly in large cap US equities, are perplexing. Although the worst-case tariff scenarios seem to be off the table, current multiples leave little room for negative surprises. Against the backdrop of slowing US growth, elevated government debt levels and sustained higher long-term interest rates, these valuations seem particularly stretched. Although valuations can stray from historical averages for extended periods, the combination of elevated valuations and a high degree of concentration creates a ripe environment for volatility.

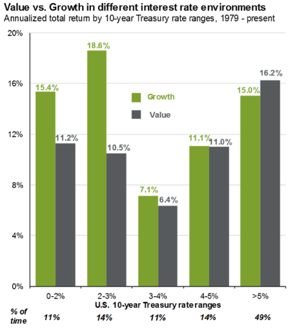

While growth equities have outperformed their value counterparts over the past decade, they haven’t historically outperformed in higher interest rate environments where the 10-year treasury yield was above 4%. We don’t advocate avoiding US large cap equities entirety. However, we firmly believe in the prudence of diversification as well as the fact that valuations matter. The present environment seems like an opportune time to review your portfolio for concentrations. The S&P 500 has not experienced positive 10-year subsequent returns when the starting valuations are at today’s levels. In addition to lofty valuations, ten companies now account for nearly 40% of the S&P 500’s market cap. While concentration isn’t inherently bad, it can set the stage for increased volatility, like we saw in April. There are several areas, including small cap domestic equities as well as international equities, where valuations are nearer to their historical averages and there is less concentration risk.

The Fed & Fixed Income

Thus far in 2025, the Fed has held the Fed Funds rate steady at 4.25-4.5%, following 100 bps of cuts in 2024. The magnitude of expected cuts this year has fluctuated wildly. Recent weakening in employment data sparked an increased expectation of cuts. Futures markets indicate that the Fed is expected to cut two to three times this year. Shelter inflation, the largest component of CPI, has continued its steady downward trend. The great unknown is to what extent the trade war will translate into additional inflationary pressure. Given uncertainty around the path of inflation and a stable labor market, the Fed is incentivized to take a wait and see approach as opposed to being overly accommodative.

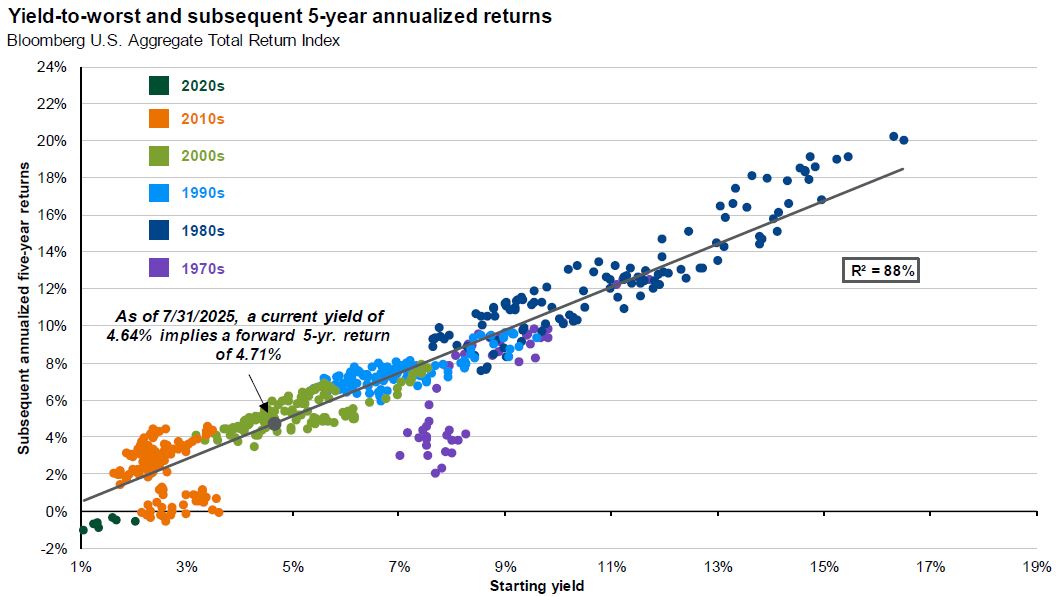

Starting yields are the best predictors of fixed income returns. The correlation between the two is typically strong, apart from periods where interest rates subsequently increased rapidly. There is some risk that long-term interest rates could trend upward, regardless of the Fed’s actions at the short end of the yield curve. This risk is primarily driven by substantial Federal debt issuance. However, elevated yields help insulate investors from potential interest rate volatility. Notably, investors no longer need to accept a yield discount to shift from cash equivalents to core fixed income. Although the Fed’s path is uncertain, the trend for short-term yields is likely to be flat to slightly downward. A few years ago, bonds provided little yield, making fixed income investors vulnerable to restrictive shifts in monetary policy. Core fixed income now offers meaningful yield as well as an avenue for capital appreciation.

As asset allocators, we’re constantly evaluating the relative attractiveness of various asset classes. Although we advocate duration extension by shifting out of cash, we’d recommend caution in credit quality, as credit spreads are narrow relative to historical averages. While there is inherent risk to all investments, the yields available in fixed income remain attractive, particularly compared to cash equivalents and the elevated valuations on offer in equities.

Municipal Bond Spotlight

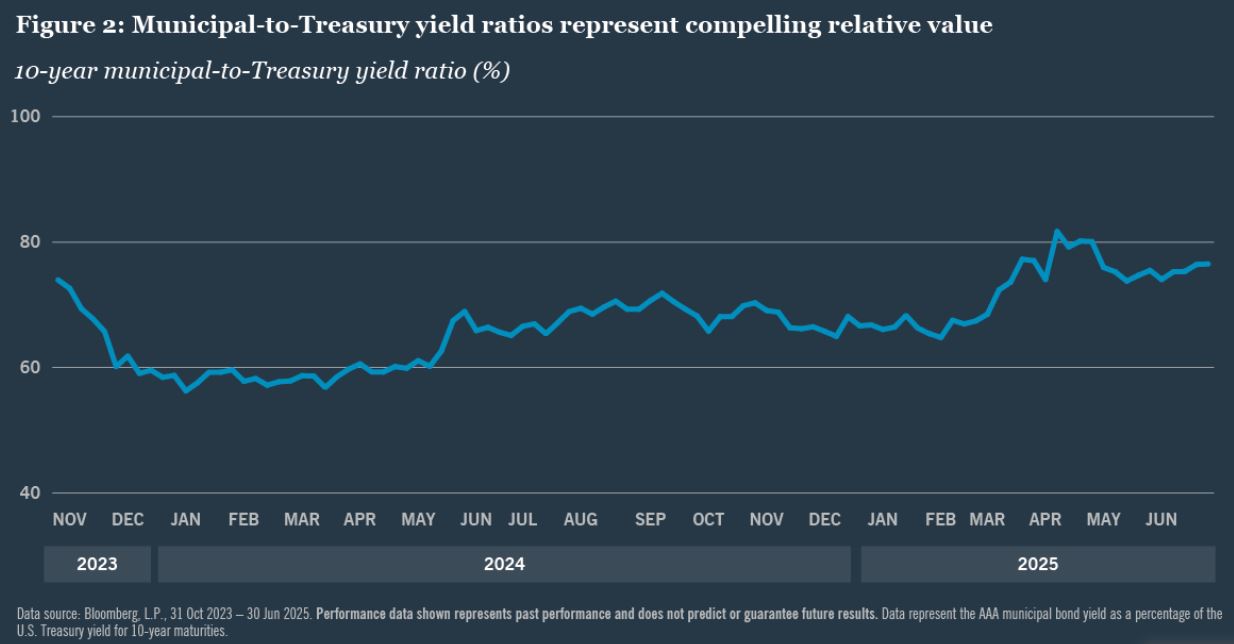

Municipal bonds represent a unique corner of the fixed income universe and 2025 has been a lackluster year for the asset class. The Bloomberg Municipal Bond Index is essentially flat for the year, while the Bloomberg Aggregate Bond Index, representing taxable bonds, is up over 4% as of mid-August. While movements in interest rates are a key driver of performance, the municipal bond market has some idiosyncrasies. The tax-exempt status that many municipal bonds enjoy means that the universe of buyers is narrower than it is for taxable bonds. Additionally, the smaller size of the municipal market makes it sensitive to changes in issuance.

This year, the performance gap between municipal bonds and their taxable counterparts has been notably wide. This poor relative performance is not likely due to credit concerns, as spreads remain narrow and municipalities are well-funded. It’s likely attributable to two factors: issuance and the retail nature of municipal markets.

Municipal issuance through July was up about 18% relative to 2024. Given the narrow municipal bond investor base, shifts in issuance can be impactful. In April, municipals didn’t see the same flight to quality as taxable bonds, placing a damper on relative performance. Although the recent technical background for municipals has been unfavorable, yields are historically attractive. Tax-equivalent yields, assuming the highest Federal tax bracket, sit near 7% for the Bloomberg Municipal Bond Index. The municipal curve has also steepened, rewarding investors for taking duration risk. These attractive yield opportunities come with minimal credit risk. The 10-year cumulative default rate for municipal bonds is about 0.16%, per Moody’s, a fraction of the 10-year cumulative corporate bond default rate. Relative to other asset classes, municipal bonds offer an attractive risk-adjusted opportunity for tax-sensitive investors.

International Equity: Diversification & Growth

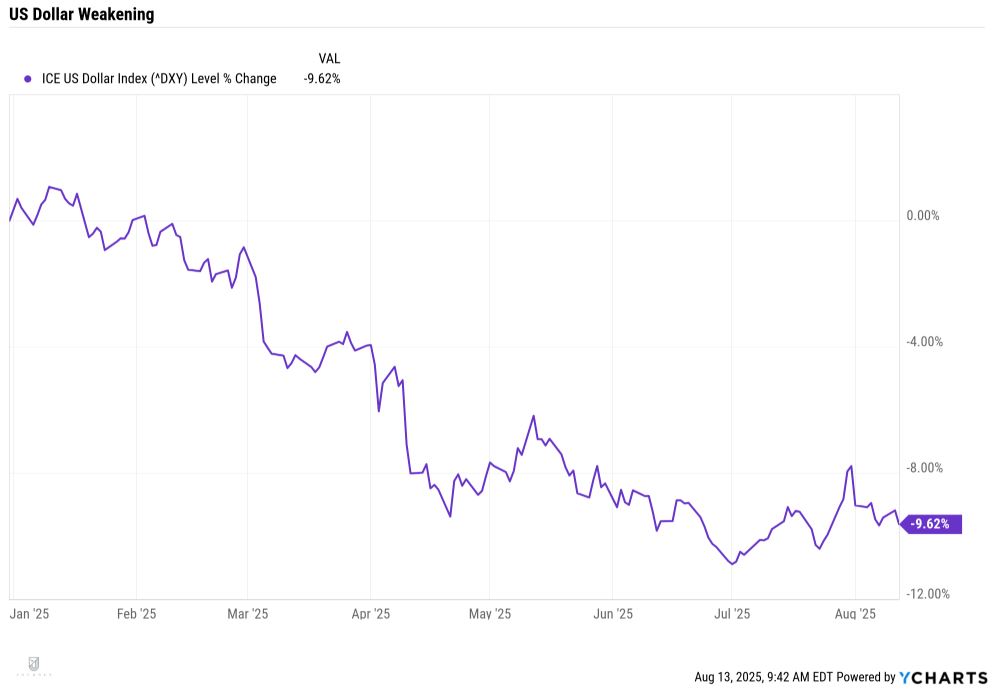

US equities outperformed their foreign counterparts over the past decade. That outperformance was built on a foundation of stable trade policy, historically low interest rates and a strong dollar. All three of those elements have shifted dramatically. While there are risks to investing globally, we believe that there is a greater risk in concentrating investment exposure domestically. The thesis for investing internationally is based on four pillars: strong fundamentals, attractive valuations, a weaker Dollar and a greater level of diversification.

While foreign businesses have been in the spotlight when the topic of tariffs is raised, many foreign firms have little US exposure. Just 22% of non-US firms’ revenues are generated in the US, making them far less vulnerable to tariff-related volatility than US companies. There are also compelling international growth trends that deserve attention and capital. Oxford Economics estimates that by 2029, over 100 million households will join the middle class in India and China alone. Outside of favorable demographic trends, China and India have shifted their economies towards the service sector over the past two decades, supporting a higher standard of living. Emerging market economies are expected to make up about 50% of global GDP in the next decade. Outside of Asia, Europe has made substantial commitments to infrastructure modernization and becoming more self-sufficient. Investment in infrastructure has historically had a multiplier effect on growth, to a greater degree than other types of public spending.

In an environment where US equities are highly concentrated in a handful of names and valuations are elevated, international equities offer diversification and attractive valuations without sacrificing growth opportunities. The first half of the year demonstrated the benefits of a globally allocated portfolio. We aren’t recommending ostracizing US equities entirely. However, we believe that a meaningful international equity allocation offers diversification and reasonable valuations in addition to exposure to attractive growth trends.

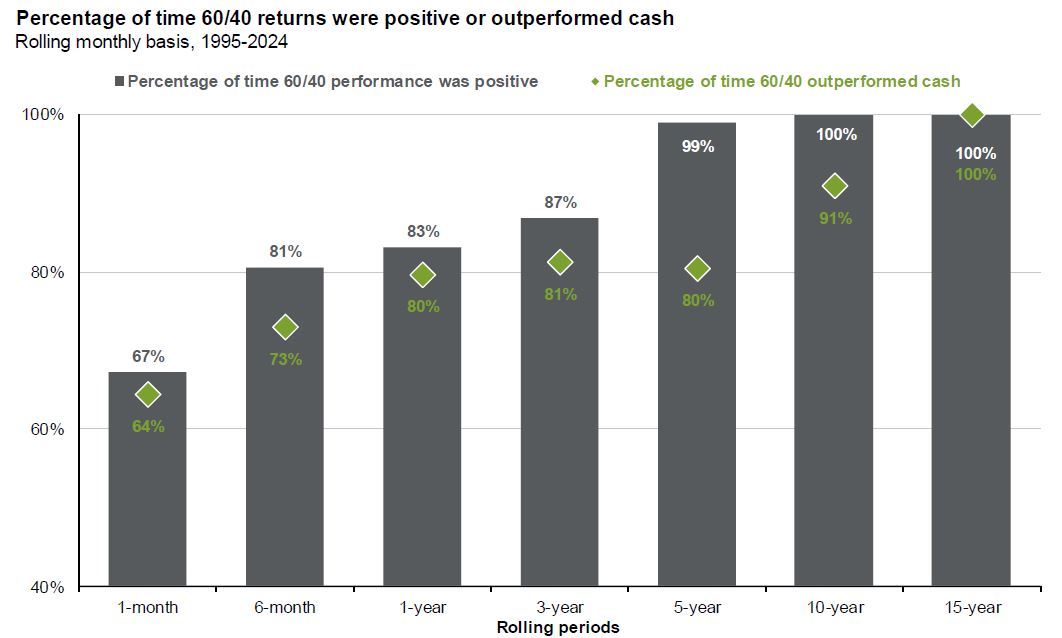

Behavioral Finance: Getting & Staying Invested

While many investors, us included, spend a substantial amount of time analyzing the economic outlook and its impact on portfolio positioning, the simplest predictor of investment success is time in the market. It nearly always feels like there may be a better time to invest, which is a belief derived from the fantasy of a perfectly timed investment. While that may sound like a prudent course, particularly given recent market performance, history tells a different story.

Over the past 30 years, a 60/40 portfolio of equities and fixed income has delivered positive performance over 99% of rolling 5-year periods. After 10 years, that improves to 100%. That portfolio also outperformed cash in over 80% of one-year periods. Although cash can feel like a haven, it rarely outperforms inflation over extended periods. While we believe valuations are a factor in the attractiveness of various market segments, picking and choosing market entry points has proven to be a fruitless exercise for investors. As such, we advocate determining cash reserves based on the needs of your personal financial plan. While it may be tempting to sit on cash during periods of uncertainty, the return drag of cash relative to other asset classes is meaningful over time.

What it All Means

Equity Valuations

US Equity markets remain highly concentrated in a handful of names. Valuations, particularly for the largest US companies, are well above historic norms. If your portfolio looks like the S&P 500, you may be more exposed to volatility than a more diversified allocation. There are several areas, including small cap domestic equities as well as international equities, where valuations are more reasonable and there is less concentration risk.

The Fed & Fixed Income

The market now anticipates two to three rate cuts this year. While inflation has remained stable, upside risk remains as the impact of tariffs is absorbed. Long-term yields are driven by dynamics in the Treasury market as well as inflation expectations. Both of those trends point towards sustained higher yields. Long-term rates sit at attractive levels. As the magnitude of expected rate cuts has risen, locking in higher long-term rates seems prudent.

Tariffs & The Economy

The impact of tariffs on equity markets is difficult to forecast, given the ever-changing proposals on the table. However, the increase in uncertainty due to trade policy is likely to dampen business activity and investment. The labor market appears weaker but stable, while the US consumer is strained. Although US growth is likely to be slower than it has been over the past decade, a gradual slowing seems more likely than a recession.

Global Opportunities

While there are risks to investing globally, we believe that there is a greater risk in concentrating investment exposure domestically. The thesis for investing internationally is based on four pillars: strong fundamentals, attractive valuations, a weaker Dollar and a greater level of diversification. A global allocation is likely better positioned to weather tariff uncertainty than a portfolio that is US-concentrated.

Relevant Disclosures: This information was prepared by FSM Wealth Advisors, LLC d/b/a Journey Wealth Management, LLC (“Journey”), a federally registered investment adviser under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Journey’s Form ADV Part 2A and Part 2B can be obtained by written request directly to: 22901 Millcreek Blvd., Suite 225, Cleveland OH 44122.

The information herein was obtained from various sources. Journey does not guarantee the accuracy or completeness of information provided by third parties. The information provided herein is provided as of the date indicated and believed to be reliable. Journey assumes no obligation to update this information, or to advise on further developments relating to it.

Investing involves the risk of loss and investors should be prepared to bear potential losses. Past performance is not indicative of future results. Neither the information nor any opinion expressed herein should be construed as solicitation to buy or sell a security or as personalized investment, tax, or legal advice. For advice specific to your situation, please consult an appropriately qualified professional investment, tax or legal adviser.

Four Pillar Friday

Stories, research, and reflections on how we spend our most important currency: TIME

Objectives-Based Investing: The Intersection of Planning & Portfolio Construction

The average investor has historically under-performed a broadly diversified portfolio dramatically. In fact, the average investor tends to under-perform even within asset classes. Why is that?

Four Pillar Friday

Stories, research, and reflections on how we spend our most important currency: TIME