Insights Blog

Quarterly Market Commentary

April 14th, 2026 // Jack LaLiberte

Market Recap

The recent turmoil in the Middle East disrupted what had been a remarkably placid 10-month period following last spring’s tariff-related volatility. Interest rates have edged higher over the past quarter, likely due to market concerns around the future path of inflation, muting recent fixed income performance. While the latest volatility has been disconcerting, a globally diversified equity portfolio has weathered geopolitical instability reasonably well. Underneath the headline performance lies a rotation, with capital shifting from domestic growth equities towards the remainder of the equity universe, including value, small caps and international equities.

Looking Ahead

While the resolution of the Iranian conflict is far from certain, the worst-case scenarios appear to have been avoided. Although oil prices have risen sharply, futures markets indicate that prices are expected to normalize in the second half of the year. In the near term, risks appear tilted towards slowing growth rather than an elevated likelihood of a recession. US GDP growth is likely to remain sluggish, due to a weaker consumer, dubious returns on AI investments and a lack of labor force growth. As we saw in 2025, the best defense against volatility is a broadly diversified portfolio. Outside of the concentrated neighborhood of US large cap growth equities, valuations are near historic norms. Fixed income yields have become even more attractive in recent weeks, particularly relative to cash. The gap between core fixed income yields and money market rates has continued to expand, rewarding investors willing to accept modest duration risk.

Asset Allocation

While geopolitical risk rose to the forefront in the first quarter, markets have demonstrated remarkable resilience. The rotation away from US growth equities likely represents a healthy reset for valuations, after the increasing concentration of the past decade. The global growth outlook appears more tepid but remains far from concerning levels. As such, we prefer to remain exposed to the largest number of potential growth catalysts, rather than betting on a single trend. Please don’t hesitate to reach out to your advisor to schedule time to discuss your financial plan, including your goals and planning assumptions. Allowing planning to drive portfolio construction, rather than market fluctuations or prognostication, helps ensure that your portfolio remains aligned with your vision for the future.

Leading Topics

Energy Shocks

While there’s been much discussion around volatile energy prices in recent weeks, context is valuable. Current price levels are far from unprecedented. In 2022, oil prices surged above $100 for several months. In 2008, prices also crested above the $100 mark. Since 2008, cumulative U.S. inflation has exceeded 50%, yet energy prices remain among the most persistent disinflationary forces of the past two decades. Additionally, the US is now a net oil exporter, to the tune of 100 million barrels in 2025. While Europe and Asia are more exposed, the shift from Russian energy dependence a few years ago provides a recent example of the flexibility of supply chains and the resilience of equity markets.

Economic Fundamentals

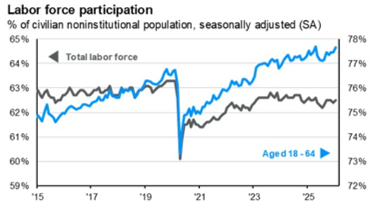

The labor market remains stable, with low levels of layoffs and hiring. The labor force participation rate has continued to climb, indicating that slower growth in the employment rolls may reflect elevated retirements rather than a lack of labor demand. The consumer has remained resilient, although discretionary spending growth has become increasingly concentrated in a narrow subset of households. If the US is to continue to expand GDP growth at a reasonable pace, productivity will need to make up for a lack of labor force expansion. The global outlook is more compelling, with the IMF estimating 3%+ growth globally in 2026.

The Federal Reserve, Inflation & Fixed Income

Expectations around Fed rate cuts have shifted dramatically in recent months. Given the potential for additional energy-related inflationary pressure, markets now expect the Fed to hold rates steady through early 2027. Longer-term rates rose modestly in the first quarter. However, higher yields help insulate fixed income investors from interest rate volatility. Given elevated equity valuations and a slower growth outlook, the opportunity set in fixed income remains compelling. We believe that a moderate approach to both duration and credit quality is called for, as the yield curve is likely to continue to steepen. Investors with outsized cash holdings are vulnerable to reinvestment risk and should consider duration extension.

Global Equity Markets

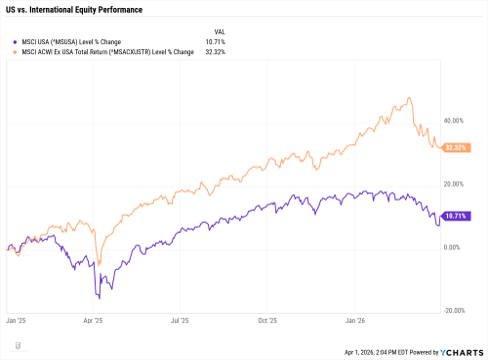

International equities outperformed their domestic counterparts by over 10% in 2025 and have continued to do so in 2026. While valuations have expanded slightly, they remain near historic averages and well below US multiples. Domestically, concentration remains a concern, with 10 companies making up nearly 40% of the S&P 500 market cap. Many of the largest U.S. companies have invested heavily in the ongoing artificial intelligence buildout. Should lofty return expectations for these investments fail to materialize at the pace that the market expects, concentrated exposure leaves investors vulnerable to outsized volatility. The narrow equity performance of the past decade was partially fueled by a strong Dollar and ultra-low interest rates. That concentrated performance may not persist if those structural trends shift. Exposure to regions with diverse tailwinds allows portfolios to better weather uncertainty and opens multiple avenues for growth.

US Economic Outlook: Tepid Resilience

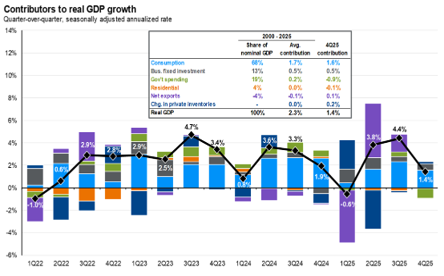

US GDP growth normalized in the fourth quarter, after experiencing some volatility over the prior three quarters due to the shifting impact of tariffs on net exports. The consumer continued to drive economic activity, as import and export flows have stabilized. Consumer health is bifurcated, with the top 10% of households by income representing over 50% of consumer spending. Lower income consumers continue to struggle as COVID-era savings have been depleted. Consumer debt has returned to pre-COVID levels while delinquencies have risen sharply. Auto loan and credit card delinquencies are near 20-year highs, signaling strain for lower income consumers. Wealthier consumers have been beneficiaries of the “wealth effect”, as unusually strong market performance in recent years has bolstered balance sheets and supported vigorous spending. While slower US growth is expected, a recession in the near term appears unlikely, given stimulative fiscal and monetary policy as well as the torrid pace of corporate investment.

While some concerns have arisen around slower job creation in recent years, the labor market has proven to be resilient, with labor force participation for workers aged 18-64 near all-time highs. The reduction in the number of jobs added has not been accompanied by a material jump in new jobless claims or a meaningful increase in the unemployment rate. As such, the unimpressive number of jobs that have been created in recent years may have more to do with structural factors rather than employers’ reticence around their growth prospects. Two structural factors are weighing on the size of the workforce: an aging population and dwindling immigration flows. While immigration figures are difficult to determine with precision, various sources indicate that between 500,000 and 1.5 million immigrants left the workforce in 2025. The domestic labor force isn’t filling the void. In 2024, about 4 million Americans turned 65, while only 3.6 million children were born. A similar level of retirements is expected to continue through at least 2027, suggesting that a shrinking labor force is likely to be a persistent trend in the coming years. Developments in the AI-sphere may aid in closing the productivity gap, although precise figures on AI productivity benefits have proven elusive.

US Equities: Valuation & Concentration

Thus far in 2026, market rotation has been the most prominent equity trend, as investors have diversified portfolios away from the largest, most growth-sensitive US companies. Portfolios that are concentrated within this narrow neighborhood have experienced substantially more volatility relative to those with broader equity exposure. The market appears to be reassessing the risk associated with elevated levels of concentration and the growth expectations embedded in some of the most highly valued companies. Despite a period of equity rotation, concentration risk remains elevated domestically, with 10 companies making up nearly 40% of the S&P 500 market cap. The valuations of the largest companies in the US are elevated relative to historical averages as well as other equity market segments. While valuations are not great predictors of short-term returns, they have a reasonable negative correlation with long-term outcomes. Historically, the S&P 500 has never experienced positive 10-year returns starting from current valuation levels. As such, we encourage you to review your equity exposure to help ensure that your allocation is adequately diversified.

Perhaps the most concerning aspect of the current concentration level in US equity markets is the fact that many of the largest US companies are relying on the same tailwinds for growth. Amazon, Nvidia, Google, Microsoft and Broadcom are heavily invested in the buildout of AI infrastructure. While artificial intelligence certainly seems like a compelling technology that provides tangible productivity benefits, it’s unlikely that every AI-related company will win the current capital investment arms race. Our concern around concentration is less a fundamental call on the prospects of these companies, but more an assessment of the risk that these equities are likely to move together during periods of market weakness. Furthermore, the sheer amount of investment in AI infrastructure, which is estimated at around $2 trillion since 2013, necessitates tremendous future incremental earnings for these firms to reap a reasonable rate of return on their investments. After all, stock prices are largely a reflection of expectations around earnings growth and persistence. While AI has caught the attention of many investors, there are plenty of quieter trends that have performed as well or better in recent years. We believe firmly in the prudence of broad diversification. There are plenty of compelling global growth opportunities that don’t rely on chasing a few concentrated names with lofty valuations.

Global Equity Opportunities

In a reversal of the trend of the past 15 years, international equities dominated their US counterparts in 2025. That outperformance continued in the first quarter. A few likely contributing factors include the concentrated and expensive nature of US equity markets, a weaker Dollar and a recognition of the growth opportunities that exist outside of the US. Additionally, a global investment approach has provided compelling diversification benefits. Adding non-US exposure is not necessarily a bet on US underperformance, but an insurance policy against the concentrated and expensive nature of US equity markets.

While Europe and Asia are more dependent on Middle Eastern oil than the US, a short-term headwind shouldn’t overshadow the long-term catalysts for international equity performance. At the macro level, international equities provide far more attractive valuations and a greater degree of diversification than their US counterparts. However, underneath the broader trend of ex-US outperformance lie numerous regional and sectoral catalysts.

In Asia, a rapidly expanding consumer class is helping to drive economic development. Chinese trade wasn’t derailed by tariffs last year. In fact, exports hit a new record high. China’s recovery is expected to be uneven as ongoing real estate stress weighs on consumer behavior. However, valuations are hard to ignore, with Chinese equities trading around 14x earnings.

In Europe, concerns around an energy-related economic slowdown are likely overstated. While GDP growth over the next few quarters is likely to be sluggish, the impact of the Russian invasion of Ukraine on energy prices was much more substantial than the worst-case ECB projections. Increased infrastructure and defense spending are likely to provide persistent growth tailwinds. Financials are the largest sector in Europe and should benefit from a steeper yield curve, while exhibiting a low sensitivity to energy costs.

In Europe, concerns around an energy-related economic slowdown are likely overstated. While GDP growth over the next few quarters is likely to be sluggish, the impact of the Russian invasion of Ukraine on energy prices was much more substantial than the worst-case ECB projections. Increased infrastructure and defense spending are likely to provide persistent growth tailwinds. Financials are the largest sector in Europe and should benefit from a steeper yield curve, while exhibiting a low sensitivity to energy costs.

Although the current geopolitical environment may prompt investors to turn inward in search of safety, international equities have provided a much less volatile experience over the past year. While no one knows what the remainder of 2026 will hold, global diversification seems prudent given the elevated valuations and substantial level of concentration present in US equity markets.

Inflation & The Federal Reserve

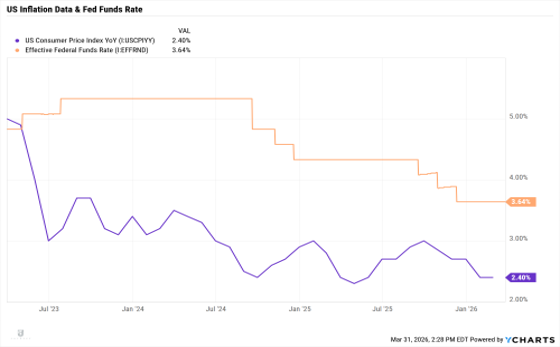

US inflation was fairly static over the past year, bouncing between 2.3% and 3%. The shelter component of inflation has continued to ease as housing supply improves. Goods and services inflation has offset much of the shelter-related improvement, keeping the headline figure range-bound. The worst of the tariff-related impacts have likely been passed through the supply chain and a re-escalation of the trade war seems unlikely given the Supreme Court’s recent decision declaring most unilateral presidentially imposed tariffs unconstitutional. Some specific tariffs were allowed to remain in place. However, the peak impact appears to have passed. In recent weeks, inflationary concerns have pivoted from trade barriers to concerns around energy prices. An increase in inflation over the next few months wouldn’t be surprising, given the sharp jump in energy costs. However, oil futures markets and 1-year inflation swaps don’t indicate that the market expects a longer-term inflationary spiral. 1-year inflation swaps are currently trading around 2.3%, indicating that although we may see a short-term jump, inflation seems likely to remain rangebound over the coming 12 months.

In 2025, the Fed eased financial conditions by cutting rates three times and by ending their quantitative tightening program. Expectations around the path of the Fed Funds rate have shifted dramatically in recent weeks. In late February, the market anticipated two to three rate cuts this year. Now, futures markets indicate that a cut this year is unlikely and there is a small chance that the Fed will raise rates in 2026. The change in Fed expectations has translated to longer-term rates, as long-term treasury yields have increased. As such, even if the Fed holds steady on short-term rates, the gap between core fixed income yields and cash equivalents has expanded. A lack of rate cuts is likely to place additional pressure on low-income consumers, given elevated levels of consumer debt. Higher rates are also likely to constrict housing market activity, which has already been limited.

Fixed Income Outlook

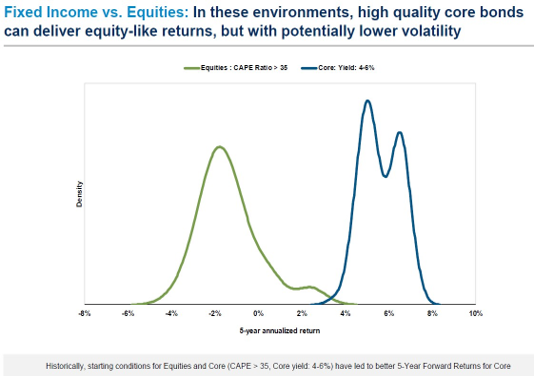

In an era of higher real rates, bonds have reprised their dual role as an income generator and a volatility mitigator. The yield curve has steepened over the past year and may continue to do so even if the Fed holds short-term rates steady. Currently, core bonds provide a yield premium of about 75 bps above money market rates. While that sounds unspectacular, the added benefit of extending duration is a reduction in reinvestment risk. Fixed income also offers a stronger inverse correlation with equities, while cash does not. Investors are no longer required to accept a yield discount to shift from cash equivalents to core fixed income, reducing the perceived friction for cash-heavy investors.

While fixed income appears benign relative to the past few decades of torrid equity market performance, there’s no guarantee that that dynamic will continue. Given elevated domestic equity valuations and a slower growth outlook, the next decade may look rather different. While equities still have their place as the long-term growth engine of your portfolio, the yields offered by fixed income are attractive on a relative basis. This is especially valuable for investors beginning to draw on their portfolios, as a balanced allocation can help mitigate sequence‑of‑return risk.

We believe that not all fixed income is created equal and that given the shifting yield curve and credit spreads, an active approach to the asset class is warranted. In equities, an index based on market cap weightings makes some logical sense. However, in fixed income, loaning the largest amounts to the entities with the most debt seems like a suboptimal capital allocation methodology. While yields and fixed income prices have proven volatile over the past few months, we believe that yields are attractive on a relative and absolute basis. The relationship between starting yields and subsequent returns has historically proven to be strong. Against the backdrop of stretched equity valuations and a slower growth outlook, fixed income yields appear particularly compelling. Investors with outsized cash holdings are vulnerable to reinvestment risk and should consider duration extension.

Behavioral Finance: Conflicts & Markets

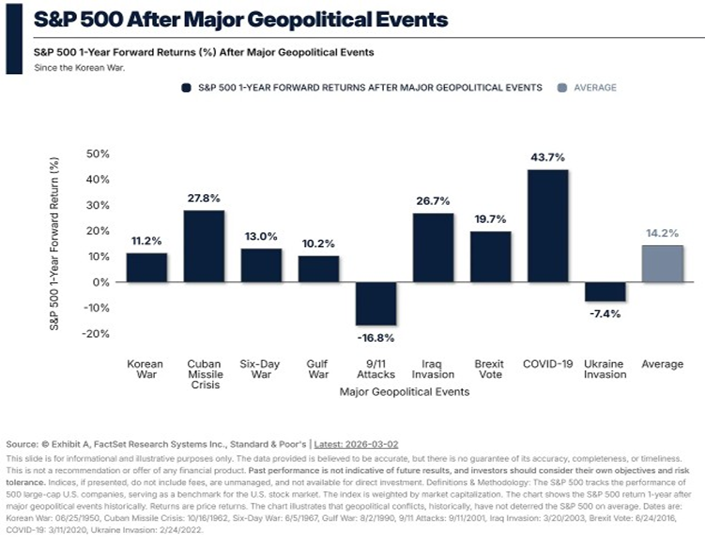

In recent weeks, geopolitical risk has bubbled to the surface as the US and Israel have taken military action against Iran. The Iranian retaliation against Israel was unsurprising. However, markets have been jarred by the scope of the retaliation and the wide-ranging consequences for regional energy flows. About 20% of the world’s oil supply travels through the Strait of Hormuz, over which Iran can exercise a large measure of control. The US is more insulated from oil price shocks than in past decades. Since 2020, the US has been a net oil exporter, with the gap between imports and exports expanding to about 100 million barrels in 2025. However, energy markets are global in nature. If supply constricts elsewhere, the impacts will likely be felt domestically. The price of energy is a factor in the production and transport of nearly every product we consume, raising concerns around inflationary risks. Those concerns have been reflected in the recent increase in yields.

While it’s easy to get caught up in the day-to-day headlines, the trajectory of global growth is unlikely to shift meaningfully due to the ongoing conflict. Last year serves as a recent example of the resilience of capital markets during periods with elevated uncertainty. While no one knows how the current conflict will ultimately play out, geopolitical events tend to have short-lived impacts on market performance.

Rather than focusing on the whims of world leaders, we recommend focusing on the controllables, which include the following:

- Is your allocation globally diversified? Regional concentration can elevate risk without increasing return expectations.

- Do you have adequate cash to fund upcoming expenses? An adequate cash cushion gives your portfolio time to work.

- Is your financial plan up to date? We find that periods of market volatility serve as an excellent opportunity to review your portfolio to help ensure that your asset allocation aligns with your goals.

We don’t recommend making major shifts to your asset allocation based solely on market movements. As we saw last year, the best course of action during many crises is simply to do nothing. Ultimately, we build plans and portfolios precisely for times like these. While the fundamentals of cash flow planning and portfolio construction seem mundane during periods of market tranquility, the comfort of having a plan and sticking to it can pay both tangible and intangible dividends during periods of instability.

What it All Means

Economic Outlook

US economic data points to a slower growth trajectory, although a recession in the near-term seems unlikely. The labor market appears stable, with slower hiring being offset by sluggish labor force growth. The consumer shows some signs of weakness, as evidenced by rising consumer debt delinquencies. If US GDP growth is to continue at a reasonable pace, productivity gains are going to have to make up for slower labor force expansion. Globally, the outlook is brighter, with growth expectations around 3%.

Fixed Income Opportunities

Core fixed income offers attractive yields without the need to accept substantial credit risk. These yields are particularly appealing on a relative basis given elevated equity valuations and diminished cash yields. Given modest yield curve steepness and tight spreads, we recommend a measured approach to duration and credit risk. Investors with outsized cash holdings are vulnerable to reinvestment risk and should consider duration extension.

Inflation & The Federal Reserve

Inflation has remained range-bound over the past year as easing shelter costs have been offset by tariff-related increases in goods prices. While concerns around energy prices are valid, the impact is likely to be short-lived. Fed expectations have shifted dramatically over the past month, as the market no longer anticipates additional easing until 2027. A lack of rate cuts is likely to place additional pressure on low-income consumers, given elevated levels of consumer debt, and may curtail housing market activity.

Equity Outlook

Thus far in 2026, market rotation has been the dominant equity trend, as investors have diversified away from the largest, most growth‑sensitive U.S. companies. The concentration risk and valuations on offer in large-cap US equities remain concerning. We believe that a meaningful allocation outside the largest S&P 500 constituents, including international and value equities, offers diversification benefits as well as exposure to a wider array of growth catalysts.

Relevant Disclosures: This information was prepared by FSM Wealth Advisors, LLC d/b/a Journey Wealth Management, LLC (“Journey”), a federally registered investment adviser under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Journey’s Form ADV Part 2A and Part 2B can be obtained by written request directly to: 22901 Millcreek Blvd., Suite 225, Cleveland OH 44122.

The information herein was obtained from various sources. Journey does not guarantee the accuracy or completeness of information provided by third parties. The information provided herein is provided as of the date indicated and believed to be reliable. Journey assumes no obligation to update this information, or to advise on further developments relating to it.

Investing involves the risk of loss and investors should be prepared to bear potential losses. Past performance is not indicative of future results. Neither the information nor any opinion expressed herein should be construed as solicitation to buy or sell a security or as personalized investment, tax, or legal advice. For advice specific to your situation, please consult an appropriately qualified professional investment, tax or legal adviser.

Quarterly Market Commentary

Equity markets in 2026 resemble a revolving door, with leadership regimes swinging wildly from small caps to value and then to growth equities. The rapid rotations we’ve witnessed over the past six months demonstrate the futility of attempting to time equity markets.

Four Pillar Friday

Stories, research, and reflections on how we spend our most important currency: TIME

Four Pillar Friday

Stories, research, and reflections on how we spend our most important currency: TIME