Insights Blog

Why Diversify?

May 12th, 2026 // Jack LaLiberte

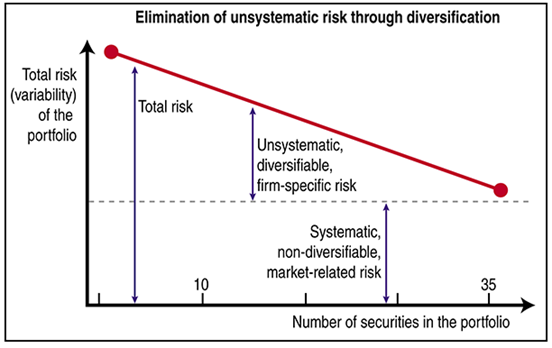

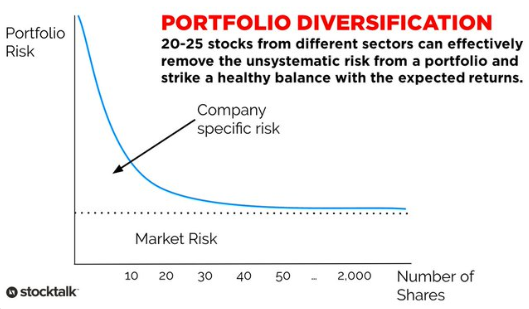

Diversification is one of the most over-used terms in the financial industry. We think it’s valuable to discuss why diversification is beneficial through multiple lenses. Let’s focus on two: the theoretical and behavioral finance rationales. The theoretical finance justification is that non-systemic risk is not rewarded. Non-systemic – or single stock – risk is the unique risk associated with a particular company. For example, if Walmart or Amazon were to be subject to a lawsuit or a product recall, that would be a company-specific risk. Systemic risk, on the other hand, is the uncertainty inherent to a broader market segment or the economy as a whole. An example would be a change in interest rates or a geopolitical shock that would impact all companies in some way. An investment’s total risk is the combination of non-systemic and systemic risks.

What does it mean when we say that non-systemic risk is not rewarded? After all, sometimes you can purchase an individual company’s stock and outperform the market over a period of time. The theoretical argument is that to do so, you would be taking on additional non-systemic risk and, as such, would not be outperforming on a risk-adjusted basis. You’re paying the same price for those shares regardless of if you purchase them individually or as part of a diversified allocation, but your risk is much higher if you only buy a few individual equities. By combining a sufficiently large portfolio of individual securities, many of the stock-specific risks offset each other and what remains is the non-diversifiable market risk. This is commonly referred to as the efficient markets hypothesis (EMH).

Diversification is cheaper and easier to achieve than ever before

Diversification is essentially free in our modern world. Investors can get exposure to a broad range of securities easily without restrictive minimums. This is due to the proliferation of pooled investment vehicles such as Exchange Traded Funds and Mutual Funds. With these products, you can eliminate non-systemic risk with minimal cost. Contrarily, systemic risk can be both challenging and costly to hedge. As such, investors demand a risk premium for holding risky asset classes. This premium varies over time and across asset classes. Historically, over the long term, fixed income tends to outperform cash and equities tend to outperform fixed income. This is partially due to the incremental systemic risk you take when you invest in fixed income over cash and when you invest in equities as opposed to fixed income. Each asset class is gradually more exposed to macroeconomic risk.

The Human Element: It’s not just about the endpoint, the smoothness of the ride matters

Behavioral finance has taught us that the endpoint of a portfolio’s expected value is not the only thing that matters. The ride is equally important. If investors were unemotional, the significance of volatility would be greatly diminished. However, most people are emotional creatures, and those emotions can lead to poor investment choices. This is supported by the fact that the average investor underperforms the average investment dramatically. The DALBAR Investor Behavior Study indicated that the average investor earned an average annual return of 2.9% for the period from 2001-2020. That slightly beat inflation but drastically underperformed a 60/40 portfolio allocated to a diverse mix of stocks and bonds. The primary goal of diversification is to reduce volatility and promote less emotional investment decisions.

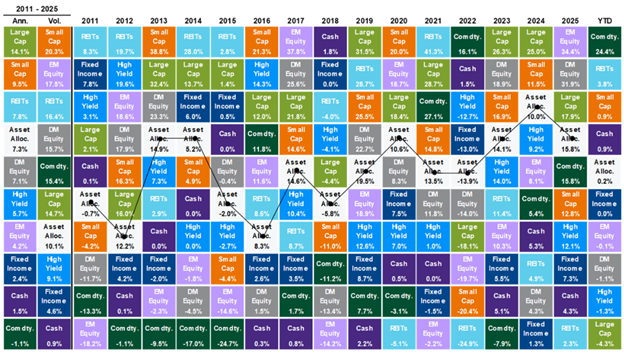

A powerful reference tool is the asset class returns “quilt” chart. This presents annual returns for a variety of asset classes and shows how they vary year to year. In addition to the individual classes, there is an “Asset Allocation” category, an artificial construct that emulates a 65/35 mix between equities and fixed income. The returns for this allocation were lower over the period than for some other categories. For example, the return for the Large Cap category was nearly double that of the Asset Allocation category over the past 15 years but the volatility was about 50% higher. It’s easy to say in retrospect that you should concentrate your portfolio in those categories that exhibited the best returns in the past. However, the ability to realize those returns is predicated on being able to ride the volatility roller coaster without getting off. If you bought and sold during the past fifteen years, your realized returns could vary dramatically from those of the category.

Conclusion & Takeaways

When a large proportion of market returns are driven by a narrow subset of securities, such as growth-oriented large cap equities, some question the benefits of diversification. Additionally, it’s often difficult to quantify risk, while returns are easy to measure. Our primary focus as asset allocators is portfolio construction, the objective of which is to maximize returns while minimizing risk. Diversification is fundamental to our approach due to both the behavioral tendencies of investors as well as the lack of compensation for taking non-systemic risk. One of the oft repeated tenets of investing is that if you’re properly diversified, you’ll always be unhappy with at least one of your investments. Said another way; if all your investments move in the same direction at the same time, you may be under-diversified. Our approach at Journey centers around evaluating your unique return requirements and risk tolerance in the context of your overall financial plan. Individual investment decisions are made with an emphasis on how the investment fits within the portfolio and, by extension, your individual financial plan, rather than in a misguided search for the next hot asset class or stock pick.

Disclosure: This information was prepared by FSM Wealth Advisors, LLC d/b/a Journey Wealth Management, LLC, a federally registered investment adviser under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply a certain level of skill or training. Neither the information presented nor any opinion expressed herein should be construed as personalized investment, financial planning, tax, or legal advice. For advice specific to your situation, please consult an appropriately qualified professional adviser(s). Certain information herein may have been obtained from various third-party sources; Journey does not guarantee the accuracy or completeness of such information. Investing involves the risk of loss and investors should be prepared to bear potential losses. Past performance is not indicative of future results.

Four Pillar Friday

Stories, research, and reflections on how we spend our most important currency: TIME

Four Pillar Friday

Stories, research, and reflections on how we spend our most important currency: TIME

Four Pillar Friday

Stories, research, and reflections on how we spend our most important currency: TIME